Quote Thief

How A Tiny Stock Exchange Earns Millions of Dollars Every Year

The New York Stock Exchange recently rebranded their NYSE Chicago exchange to NYSE Texas. If you’re like most people, you have never heard of the NYSE Chicago or even knew that the NYSE owns a total of five of the current sixteen U.S. stock exchanges.

What was the NYSE Chicago?

The NYSE acquired the Chicago Stock Exchange in 2018 and rebranded it to NYSE Chicago. Since then, the exchange has languished with a market share of less than 1%. But under the rules of Reg NMS, lack of market share doesn’t mean lack of revenue for the exchange.

When Reg NMS was implemented in 2007, the SEC changed the way exchanges allocate the market data revenue that is collected from stock market investors. Approximately $400 million is split annually amongst the exchanges and the trade reporting facilities based on a formula which allocates 50% for trades and 50% for quotes. According to the NYSE , here is how this works:

The Revenue Allocation Rule sets forth a two-step process to allocate Plan revenue among CTA and UTP Plan Participants.

• The first step is to identify the revenue attributable to each Eligible Security in the Network’s data stream (the “Security Income Allocation” or “SIA”).

• The second step is to identify the Participant’s share of revenue in an Eligible Security based on the “Trading Share” and “Quoting Share” of each Participant. 50% of the SIA is allocated to Participants based on their respective Trading Share and 50% of the SIA is allocated to the Participants based on their respective Quoting Share.

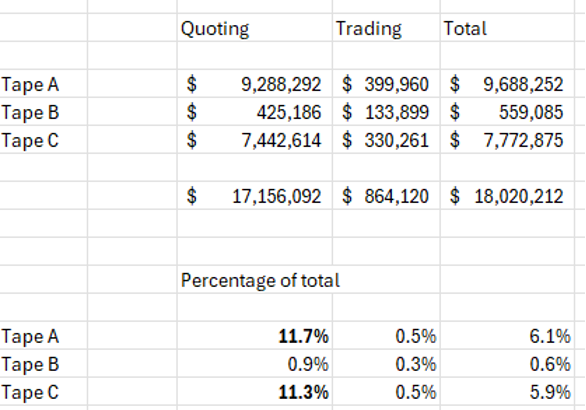

Considering their tiny market share, you might think that market data revenue would not be a major source of revenue for the NYSE Chicago. However, NYSE Chicago generated an enormous number of quotes which added up to millions of dollars of revenue for the exchange. The chart below shows that NYSE Chicago earned over $17 million in quote revenue in 2024, not bad for an exchange that has 0.5% market share.

In addition to the large amount of quotes relative to their market share, NYSE Chicago also has an enormous amount of cancellations. The chart below shows that their cancel to trade ratio is more than 250-1, compared to NYSE which is 13-1 and Nasdaq which is 20-1.

Is an exchange that cancels most of their orders adding any value to the investment process? Should exchanges with less than 1% market share be allowed to continue to have a protected quote? Maybe it’s time for the SEC to revisit the market data revenue formula.

Joe is a pleasure to read.

Hard to argue with this.